⏱️ Time Series Features

Time Series Features in KDP

Transform temporal data with powerful lag features, moving averages, differencing, rolling statistics, wavelet transforms, statistical features, and calendar features.

📋 Overview

Time series features enable processing of chronological data by creating transformations that capture temporal patterns and relationships. KDP provides specialized layers for common time series operations that maintain data ordering while enabling advanced machine learning on sequential data.

🚀 Types of Time Series Transformations

| Transformation | Purpose | Example | When to Use |

|---|---|---|---|

Lag Features |

Create features from past values | Yesterday's sales, last week's sales | When past values help predict future ones |

Rolling Statistics |

Compute statistics over windows | 7-day average, 30-day standard deviation | When trends or volatility matter |

Differencing |

Calculate changes between values | Day-over-day change in price | When changes are more important than absolute values |

Moving Averages |

Smooth data over time | 7-day, 14-day, 28-day moving averages | When you need to reduce noise and focus on trends |

Wavelet Transforms |

Multi-resolution analysis of time series | Extracting coefficients at different scales | When you need to analyze signals at multiple scales or frequencies |

Statistical Features |

Extract comprehensive statistical features | Mean, variance, kurtosis, entropy, peaks | When you need a rich set of features summarizing time series properties |

Calendar Features |

Extract date and time components | Day of week, month, is_weekend, seasonality | When seasonal patterns related to calendar time are relevant |

📝 Basic Usage

There are two ways to define time series features in KDP:

Option 1: Using Feature Type Directly

from kdp import PreprocessingModel, FeatureType

# Define features with simple types

features = {

"sales": FeatureType.TIME_SERIES, # Basic time series feature

"date": FeatureType.DATE, # Date feature for sorting

"store_id": FeatureType.STRING_CATEGORICAL # Grouping variable

}

# Create preprocessor

preprocessor = PreprocessingModel(

path_data="sales_data.csv",

features_specs=features

)

Option 2: Using TimeSeriesFeature Class (Recommended)

from kdp import PreprocessingModel, TimeSeriesFeature

# Create a time series feature for daily sales data

sales_ts = TimeSeriesFeature(

name="sales",

# Sort by date column to ensure chronological order

sort_by="date",

# Group by store to handle multiple time series

group_by="store_id",

# Create lag features for yesterday, last week, and two weeks ago

lag_config={

"lags": [1, 7, 14],

"drop_na": True,

"fill_value": 0.0,

"keep_original": True

}

)

# Define features using both approaches

features = {

"sales": sales_ts,

"date": "DATE", # String shorthand for date feature

"store_id": "STRING_CATEGORICAL" # String shorthand for categorical

}

# Create preprocessor

preprocessor = PreprocessingModel(

path_data="sales_data.csv",

features_specs=features

)

🧠 Advanced Configuration

For comprehensive time series processing, configure multiple transformations in a single feature:

from kdp import TimeSeriesFeature, PreprocessingModel

# Complete time series configuration with multiple transformations

sales_feature = TimeSeriesFeature(

name="sales",

# Data ordering configuration

sort_by="date", # Column to sort by

sort_ascending=True, # Sort chronologically

group_by="store_id", # Group by store

# Lag feature configuration

lag_config={

"lags": [1, 7, 14, 28], # Previous day, week, 2 weeks, 4 weeks

"drop_na": True, # Remove rows with insufficient history

"fill_value": 0.0, # Value for missing lags if drop_na=False

"keep_original": True # Include original values

},

# Rolling statistics configuration

rolling_stats_config={

"window_size": 7, # 7-day rolling window

"statistics": ["mean", "std", "min", "max"], # Statistics to compute

"window_stride": 1, # Move window by 1 time step

"drop_na": True # Remove rows with insufficient history

},

# Differencing configuration

differencing_config={

"order": 1, # First-order differencing (t - (t-1))

"drop_na": True, # Remove rows with insufficient history

"fill_value": 0.0, # Value for missing diffs if drop_na=False

"keep_original": True # Include original values

},

# Moving average configuration

moving_average_config={

"periods": [7, 14, 28], # Weekly, bi-weekly, monthly averages

"drop_na": True, # Remove rows with insufficient history

"pad_value": 0.0 # Value for padding if drop_na=False

},

# Wavelet transform configuration

wavelet_transform_config={

"levels": 3, # Number of decomposition levels

"window_sizes": [4, 8, 16], # Optional custom window sizes for each level

"keep_levels": "all", # Which levels to keep (all or specific indices)

"flatten_output": True, # Whether to flatten multi-level output

"drop_na": True # Handle missing values

},

# TSFresh statistical features configuration

tsfresh_feature_config={

"features": ["mean", "std", "min", "max", "median"], # Features to extract

"window_size": None, # Window size (None for entire series)

"stride": 1, # Stride for sliding window

"drop_na": True, # Handle missing values

"normalize": False # Whether to normalize features

},

# Calendar feature configuration for date input

calendar_feature_config={

"features": ["month", "day", "day_of_week", "is_weekend"], # Features to extract

"cyclic_encoding": True, # Use cyclic encoding for cyclical features

"input_format": "%Y-%m-%d", # Input date format

"normalize": True # Whether to normalize outputs

}

)

# Create features dictionary

features = {

"sales": sales_feature,

"date": "DATE",

"store_id": "STRING_CATEGORICAL"

}

# Create preprocessor with time series feature

preprocessor = PreprocessingModel(

path_data="sales_data.csv",

features_specs=features

)

⚙️ Key Configuration Parameters

| Parameter | Description | Default | Notes |

|---|---|---|---|

sort_by |

Column used for ordering data | Required | Typically a date or timestamp column |

sort_ascending |

Sort direction | True | True for oldest→newest, False for newest→oldest |

group_by |

Column for grouping multiple series | None | Optional, for handling multiple related series |

lags |

Time steps to look back | None | List of integers, e.g. [1, 7] for yesterday and last week |

window_size |

Size of rolling window | 7 | Number of time steps to include in window |

statistics |

Rolling statistics to compute | ["mean"] | Options: "mean", "std", "min", "max", "sum" |

order |

Differencing order | 1 | 1=first difference, 2=second difference, etc. |

periods |

Moving average periods | None | List of integers, e.g. [7, 30] for weekly and monthly |

levels |

Number of wavelet decomposition levels | 3 | Higher values capture more scales of patterns |

window_sizes |

Custom window sizes for wavelet transform | None | Optional list of sizes, e.g. [4, 8, 16] |

tsfresh_features |

Statistical features to extract | ["mean", "std", "min", "max", "median"] | List of statistical features to compute |

calendar_features |

Calendar components to extract | ["month", "day", "day_of_week", "is_weekend"] | Date-based features extracted from timestamp |

cyclic_encoding |

Use sine/cosine encoding for cyclical features | True | Better captures cyclical nature of time features |

drop_na |

Remove rows with insufficient history | True | Set to False to keep all rows with padding |

💡 Powerful Features

🔄 Automatic Data Ordering

KDP automatically handles the correct ordering of time series data:

from kdp import TimeSeriesFeature, PreprocessingModel

# Define a time series feature with automatic ordering

sales_ts = TimeSeriesFeature(

name="sales",

# Specify which column contains timestamps/dates

sort_by="timestamp",

# Sort in ascending order (oldest first)

sort_ascending=True,

# Group by store to create separate series per store

group_by="store_id",

# Simple lag configuration

lag_config={"lags": [1, 7]}

)

# Create features dictionary

features = {

"sales": sales_ts,

"timestamp": "DATE",

"store_id": "STRING_CATEGORICAL"

}

# Even with shuffled data, KDP will correctly order the features

preprocessor = PreprocessingModel(

path_data="shuffled_sales_data.csv",

features_specs=features

)

# The preprocessor handles ordering before applying transformations

model = preprocessor.build_preprocessor()

🌊 Wavelet Transform Analysis

Extract multi-resolution features from time series data:

from kdp import TimeSeriesFeature, PreprocessingModel

# Define a feature with wavelet transform

sensor_data = TimeSeriesFeature(

name="sensor_readings",

sort_by="timestamp",

# Wavelet transform configuration

wavelet_transform_config={

"levels": 3, # Number of decomposition levels

"window_sizes": [4, 8, 16], # Increasing window sizes for multi-scale analysis

"keep_levels": "all", # Keep coefficients from all levels

"flatten_output": True # Flatten coefficients into feature vector

}

)

# Create features dictionary

features = {

"sensor_readings": sensor_data,

"timestamp": "DATE"

}

# Create preprocessor for signal analysis

preprocessor = PreprocessingModel(

path_data="sensor_data.csv",

features_specs=features

)

# The wavelet transform decomposes the signal into different frequency bands,

# helping to identify patterns at multiple scales

📊 Statistical Feature Extraction

Automatically extract rich statistical features from time series:

from kdp import TimeSeriesFeature, PreprocessingModel

# Define a feature with statistical features extraction

ecg_data = TimeSeriesFeature(

name="ecg_signal",

sort_by="timestamp",

# Statistical feature extraction

tsfresh_feature_config={

"features": [

"mean", "std", "min", "max", "median",

"abs_energy", "count_above_mean", "count_below_mean",

"kurtosis", "skewness"

],

"window_size": 100, # Extract features from windows of 100 points

"stride": 50, # Slide window by 50 points

"normalize": True # Normalize extracted features

}

)

# Create features dictionary

features = {

"ecg_signal": ecg_data,

"timestamp": "DATE",

"patient_id": "STRING_CATEGORICAL"

}

# Create preprocessor

preprocessor = PreprocessingModel(

path_data="ecg_data.csv",

features_specs=features

)

# The statistical features capture important characteristics of the signal

# without requiring domain expertise to manually design features

📅 Calendar Feature Integration

Extract and encode calendar features directly from date inputs:

from kdp import TimeSeriesFeature, PreprocessingModel

# Define a feature with calendar feature extraction

traffic_data = TimeSeriesFeature(

name="traffic_volume",

sort_by="timestamp",

group_by="location_id",

# Lag features for short-term patterns

lag_config={"lags": [1, 2, 3, 24, 24*7]}, # Hours back

# Calendar features for temporal patterns

calendar_feature_config={

"features": [

"month", "day_of_week", "hour", "is_weekend",

"is_month_start", "is_month_end"

],

"cyclic_encoding": True, # Use sine/cosine encoding for cyclical features

"input_format": "%Y-%m-%d %H:%M:%S" # Datetime format

}

)

# Create features dictionary

features = {

"traffic_volume": traffic_data,

"timestamp": "DATE",

"location_id": "STRING_CATEGORICAL"

}

# Create preprocessor for traffic prediction

preprocessor = PreprocessingModel(

path_data="traffic_data.csv",

features_specs=features

)

# Calendar features automatically capture important temporal patterns

# like rush hour traffic, weekend effects, and monthly patterns

🔧 Real-World Examples

📈 Retail Sales Forecasting

from kdp import PreprocessingModel, TimeSeriesFeature, DateFeature, CategoricalFeature

# Define features for sales forecasting

features = {

# Time series features for sales data

"sales": TimeSeriesFeature(

name="sales",

sort_by="date",

group_by="store_id",

# Recent sales and same period in previous years

lag_config={

"lags": [1, 2, 3, 7, 14, 28, 365, 365+7],

"keep_original": True

},

# Weekly and monthly trends

rolling_stats_config={

"window_size": 7,

"statistics": ["mean", "std", "min", "max"]

},

# Day-over-day changes

differencing_config={

"order": 1,

"keep_original": True

},

# Weekly, monthly, quarterly smoothing

moving_average_config={

"periods": [7, 30, 90]

},

# Calendar features for seasonal patterns

calendar_feature_config={

"features": ["month", "day_of_week", "is_weekend", "is_holiday"],

"cyclic_encoding": True

}

),

# Store features

"store_id": CategoricalFeature(

name="store_id",

embedding_dim=8

),

# Product category

"product_category": CategoricalFeature(

name="product_category",

embedding_dim=8

)

}

# Create preprocessor

sales_forecaster = PreprocessingModel(

path_data="sales_data.csv",

features_specs=features,

output_mode="concat"

)

# Build preprocessor

result = sales_forecaster.build_preprocessor()

📊 Stock Price Analysis with Advanced Features

from kdp import PreprocessingModel, TimeSeriesFeature, NumericalFeature, CategoricalFeature

# Define features for financial analysis

features = {

# Price as time series

"price": TimeSeriesFeature(

name="price",

sort_by="date",

group_by="ticker",

# Recent prices and historical patterns

lag_config={

"lags": [1, 2, 3, 5, 10, 20, 60], # Days back

"keep_original": True

},

# Trend analysis

rolling_stats_config={

"window_size": 20, # Trading month

"statistics": ["mean", "std", "min", "max"]

},

# Multi-scale price patterns with wavelet transform

wavelet_transform_config={

"levels": 3, # Capture short, medium, and long-term patterns

"flatten_output": True

},

# Statistical features for price characteristics

tsfresh_feature_config={

"features": ["mean", "variance", "skewness", "kurtosis",

"abs_energy", "count_above_mean", "longest_strike_above_mean"]

}

),

# Volume information

"volume": TimeSeriesFeature(

name="volume",

sort_by="date",

group_by="ticker",

lag_config={"lags": [1, 5, 20]},

rolling_stats_config={

"window_size": 20,

"statistics": ["mean", "std"]

}

),

# Market cap

"market_cap": NumericalFeature(name="market_cap"),

# Sector/industry

"sector": CategoricalFeature(

name="sector",

embedding_dim=12

),

# Date feature with calendar effects

"date": TimeSeriesFeature(

name="date",

calendar_feature_config={

"features": ["month", "day_of_week", "is_month_start", "is_month_end", "quarter"],

"cyclic_encoding": True

}

)

}

# Create preprocessor for stock price prediction

stock_predictor = PreprocessingModel(

path_data="stock_data.csv",

features_specs=features,

output_mode="concat"

)

⚕️ Patient Monitoring with Advanced Features

from kdp import PreprocessingModel, TimeSeriesFeature, NumericalFeature, CategoricalFeature

# Define features for patient monitoring

features = {

# Vital signs as time series

"heart_rate": TimeSeriesFeature(

name="heart_rate",

sort_by="timestamp",

group_by="patient_id",

# Recent measurements

lag_config={

"lags": [1, 2, 3, 6, 12, 24], # Hours back

"keep_original": True

},

# Short and long-term trends

rolling_stats_config={

"window_size": 6, # 6-hour window

"statistics": ["mean", "std", "min", "max"]

},

# Extract rich statistical features automatically

tsfresh_feature_config={

"features": ["mean", "variance", "abs_energy", "count_above_mean",

"skewness", "kurtosis", "maximum", "minimum"],

"window_size": 24 # 24-hour window for comprehensive analysis

},

# Multi-scale analysis for pattern detection

wavelet_transform_config={

"levels": 2,

"flatten_output": True

}

),

# Blood pressure

"blood_pressure": TimeSeriesFeature(

name="blood_pressure",

sort_by="timestamp",

group_by="patient_id",

lag_config={

"lags": [1, 6, 12, 24]

},

rolling_stats_config={

"window_size": 12, # 12-hour window

"statistics": ["mean", "std"]

},

# Extract statistical patterns

tsfresh_feature_config={

"features": ["mean", "variance", "maximum", "minimum"]

}

),

# Body temperature

"temperature": TimeSeriesFeature(

name="temperature",

sort_by="timestamp",

group_by="patient_id",

lag_config={

"lags": [1, 2, 6, 12]

},

rolling_stats_config={

"window_size": 6,

"statistics": ["mean", "min", "max"]

}

),

# Patient demographics

"age": NumericalFeature(name="age"),

"gender": CategoricalFeature(name="gender"),

"diagnosis": CategoricalFeature(

name="diagnosis",

embedding_dim=16

),

# Time information with calendar features

"timestamp": TimeSeriesFeature(

name="timestamp",

calendar_feature_config={

"features": ["hour", "day_of_week", "is_weekend", "month"],

"cyclic_encoding": True,

"normalize": True

}

)

}

# Create preprocessor for patient risk prediction

patient_monitor = PreprocessingModel(

path_data="patient_data.csv",

features_specs=features,

output_mode="concat"

)

# The combination of lag features, statistical features, and wavelet transform

# enables detection of complex patterns in vital signs, while calendar features

# capture temporal variations in patient condition by time of day and day of week

💎 Pro Tips

🔍 Choose Meaningful Lag Features

When selecting lag indices, consider domain knowledge about your data:

- For daily data: include 1 (yesterday), 7 (last week), and 30 (last month)

- For hourly data: include 1, 24 (same hour yesterday), 168 (same hour last week)

- For seasonal patterns: include 365 (same day last year) for annual data

- For quarterly financials: include 1, 4 (same quarter last year)

This captures daily, weekly, and seasonal patterns that might exist in your data.

📊 Combine Multiple Transformations

Different time series transformations capture different aspects of your data:

- Lag features: Capture direct dependencies on past values

- Rolling statistics: Capture trends and volatility

- Differencing: Captures changes and removes trend

- Moving averages: Smooths noise and highlights trends

Using these together creates a rich feature set that captures various temporal patterns.

⚠️ Handle the Cold Start Problem

New time series may not have enough history for lag features:

# Gracefully handle new entities with insufficient history

sales_ts = TimeSeriesFeature(

name="sales",

sort_by="date",

group_by="store_id",

lag_config={

"lags": [1, 7],

"drop_na": False, # Keep rows with missing lags

"fill_value": 0.0 # Use 0 for missing values

}

)

# Alternative approach for handling new stores

features = {

"sales": sales_ts,

"store_age": NumericalFeature(name="store_age"), # Track how long the store has existed

"date": "DATE",

"store_id": "STRING_CATEGORICAL"

}

🔬 Advanced Time Series Feature Engineering

The new advanced time series features provide powerful tools for extracting patterns:

- Wavelet Transforms: Ideal for capturing multi-scale patterns and transient events. Use higher levels (3-5) for more decomposition detail.

- Statistical Features: The TSFresh-inspired features automatically extract a comprehensive set of statistical descriptors that would be time-consuming to calculate manually.

- Calendar Features: Combine with cyclic encoding to properly represent the circular nature of time (e.g., December is close to January).

For optimal results, combine these advanced features with traditional ones:

# Comprehensive time series feature engineering

sensor_feature = TimeSeriesFeature(

name="sensor_data",

sort_by="timestamp",

# Traditional features

lag_config={"lags": [1, 2, 3]},

rolling_stats_config={"window_size": 10, "statistics": ["mean", "std"]},

# Advanced features

wavelet_transform_config={"levels": 3},

tsfresh_feature_config={"features": ["mean", "variance", "abs_energy"]},

calendar_feature_config={"features": ["hour", "day_of_week"]}

)

# This combination captures temporal dependencies (lags),

# local statistics (rolling stats), multi-scale patterns (wavelets),

# global statistics (tsfresh), and temporal context (calendar)

📊 Model Architecture Diagrams

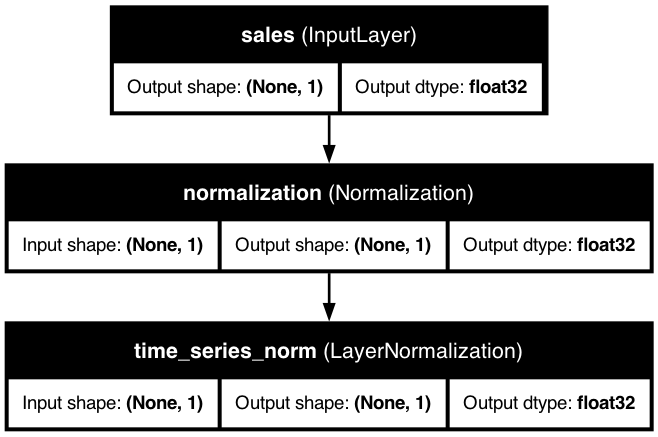

Basic Time Series Feature

A basic time series feature with date sorting and group handling, showing how KDP integrates time series data with date features and categorical grouping variables.

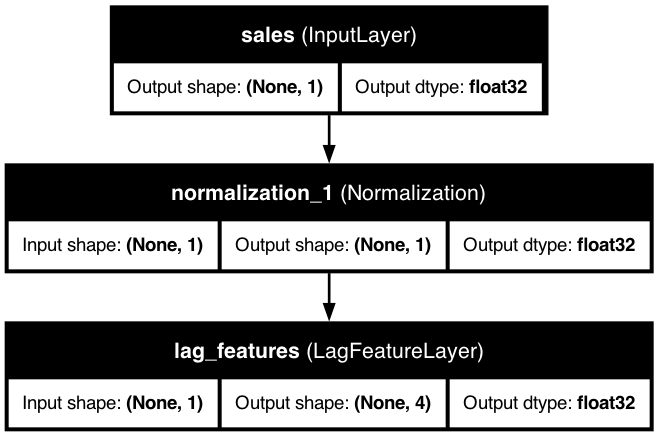

Time Series with Lag Features

This diagram shows how lag features are integrated into the preprocessing model, allowing the model to access historical values from previous time steps.

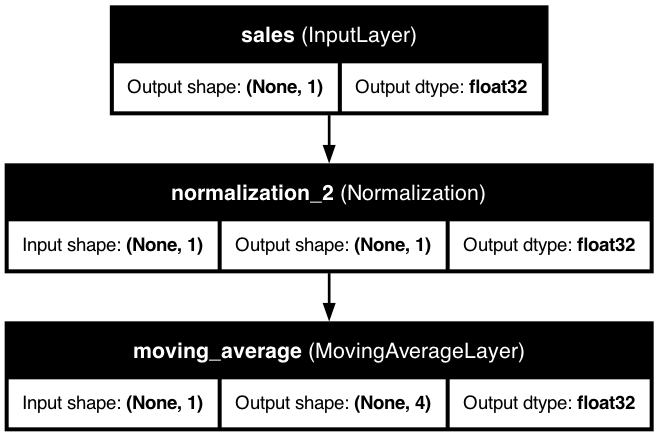

Time Series with Moving Averages

Moving averages smooth out noise in the time series data, highlighting underlying trends. This diagram shows how KDP implements moving average calculations in the preprocessing pipeline.

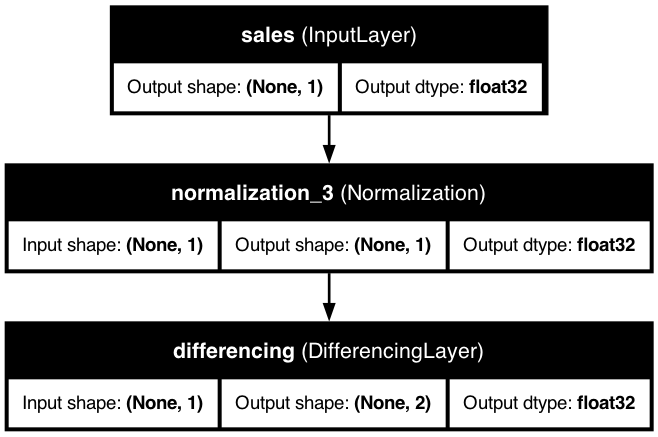

Time Series with Differencing

Differencing captures changes between consecutive time steps, helping to make time series stationary. This diagram shows the implementation of differencing in the KDP architecture.

Time Series with All Features

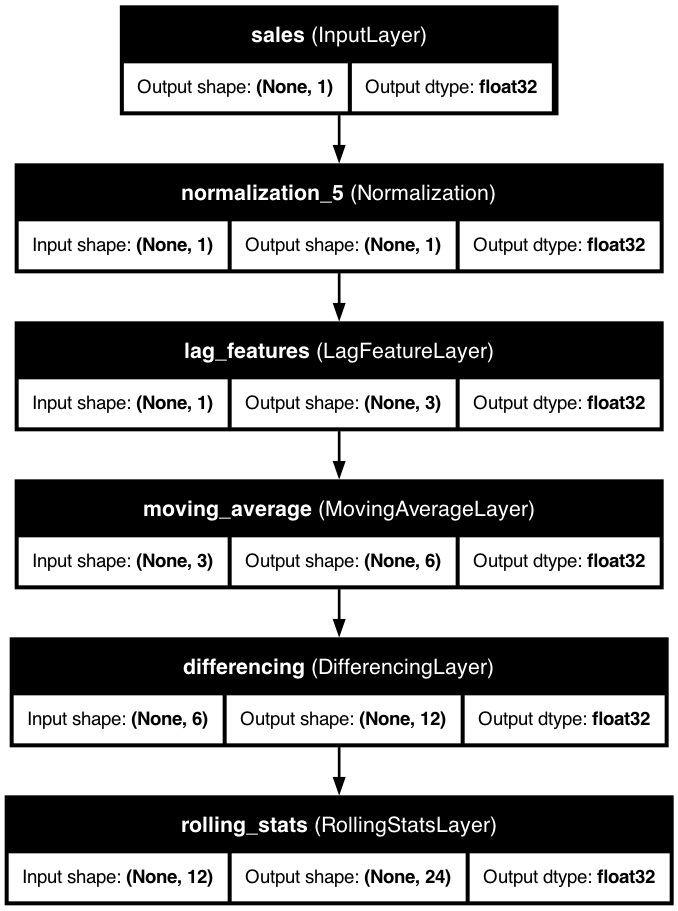

A comprehensive time series preprocessing pipeline that combines lag features, rolling statistics, differencing, and moving averages to capture all aspects of the temporal patterns in the data.

🔗 Related Topics

🔍 Inference with Time Series Features

Time series preprocessing requires special consideration during inference. Unlike static features, time series transformations depend on historical data and context.

Minimal Requirements for Inference

| Transformation | Minimum Data Required | Notes |

|---|---|---|

Lag Features |

max(lags) previous time points | If largest lag is 14, you need 14 previous data points |

Rolling Statistics |

window_size previous points | For a 7-day window, you need 7 previous points |

Differencing |

order previous points | First-order differencing requires 1 previous point |

Moving Averages |

max(periods) previous points | For periods [7,14,28], you need 28 previous points |

Wavelet Transform |

2^levels previous points | For 3 levels, you need at least 8 previous points |

Example: Single-Point Inference

For single-point or incremental inference with time series features:

# INCORRECT - Will fail with time series features

single_point = {"date": "2023-06-01", "store_id": "Store_1", "sales": 150.0}

prediction = model.predict(single_point) # ❌ Missing historical context

# CORRECT - Include historical context

inference_data = {

"date": ["2023-05-25", "2023-05-26", ..., "2023-06-01"], # Include history

"store_id": ["Store_1", "Store_1", ..., "Store_1"], # Same group

"sales": [125.0, 130.0, ..., 150.0] # Historical values

}

prediction = model.predict(inference_data) # ✅ Last row will have prediction

Strategies for Ongoing Predictions

For forecasting multiple steps into the future:

# Multi-step forecasting with KDP

import pandas as pd

# 1. Start with historical data

history_df = pd.DataFrame({

"date": pd.date_range("2023-01-01", "2023-05-31"),

"store_id": "Store_1",

"sales": historical_values # Your historical data

})

# 2. Create future dates to predict

future_dates = pd.date_range("2023-06-01", "2023-06-30")

forecast_horizon = len(future_dates)

# 3. Initialize with history

working_df = history_df.copy()

# 4. Iterative forecasting

for i in range(forecast_horizon):

# Prepare next date to forecast

next_date = future_dates[i]

next_row = pd.DataFrame({

"date": [next_date],

"store_id": ["Store_1"],

"sales": [None] # Unknown value we want to predict

})

# Add to working data

temp_df = pd.concat([working_df, next_row])

# Make prediction (returns all rows, take last one)

prediction = model.predict(temp_df).iloc[-1]["sales"]

# Update the working dataframe with the prediction

next_row["sales"] = prediction

working_df = pd.concat([working_df, next_row])

# Final forecast is in the last forecast_horizon rows

forecast = working_df.tail(forecast_horizon)

Key Considerations for Inference

- Group Integrity: Maintain the same groups used during training

- Chronological Order: Ensure data is properly sorted by time

- Sufficient History: Provide enough history for each group

- Empty Fields: For auto-regressive forecasting, leave future values as None or NaN

- Overlapping Windows: For multi-step forecasts, consider whether predictions should feed back as inputs